grow yourself and your business mindfully

Life is like riding a bicycle. To keep your balance you must keep moving.

ALBERT EINSTEIN

In this chapter, we're going to talk about what comes after you're profitable and have an organically growing customer base. For some of you, this will be relevant right this second, but even if you're not there yet, don't skip over this part. It will save you a lot of heartbreak if you can start thinking now about how to grow sustainably while avoiding some of the most common mistakes founders make.

You may be earning a nice living for yourself and your family, and in theory, your journey and the journey of your company could be coming to a close. But for many, including me, the point is not to create a lifestyle business, retire on a beach somewhere, and be done with it. The reasons to grow are different for every founder. Even though I got comfortable with the non-unicorn outcome for Gumroad in 2019, I've continued to invest in its growth. For one, it's fun and satisfying to work on a continuously improving project. Two, it feels good to find new ways to create value for our creators.

And frankly, staying put doesn't work. The world is constantly changing, and we and our businesses have to change with it. Staying put is a great way to start going backwards. You don't need to grow like crazy, but you also don't want to grow stagnant.

I've seen this play out at many companies. They solve the problem, get complacent, and over the years their customers churn and the people they hire are no longer fired up. But being a minimalist entrepreneur isn't just about owning a business that doesn't own you; it's also about owning a business that you want to work on, even if you don't have to work on it anymore.

At this stage, the real question is: How can I grow with intent, without jeopardizing the impact I make for my customers or damaging the life I've built? On the surface, it might seem straightforward to stay the course when you start to see results, but slow, sustained growth is its own kind of challenge that requires deliberate, conscious decision making.

When businesses fail, it's unlikely that a tornado of unforeseeable misfortunes is the cause. Instead, it's usually one or more of the same handful of mistakes: overspending on inventory and office space, hiring too quickly, cofounder infighting. I'll talk about how to avoid those mistakes, but also about how to deal with them because it's likely that some of them will happen to you, even if you try to avoid them.

There are two categories of self-inflicted mistakes, or 'unforced errors,' to watch out for. The first set relates to running out of money, and the second set to running out of energy.

Let's start with some basic economics and go from there.

Don't Spend Money You Don't Have

The most important equation in business: profit equals revenue minus costs.

It sounds so simple: Make more than you spend, and your company can keep on going forever. Make less than you spend, and you will eventually fail.

But you'd be surprised how often founders ignore profitability (read: sustainability) and focus on product development, growing, hiring, and all kinds of other things, right up until the money runs out. Paul Graham, founder of Y Combinator, can size up a company immediately based on whether they're 'default alive or default dead.' If expenses and revenues stay constant, will the company live or die? Incredibly, half of the founders he talks to have no idea.

In Graham's experience, the founders don't know because they don't think they need to know. They're counting on investors to swoop in and save them if things go south. But if you're bootstrapping your company, you have to watch your own balance sheet because there's no one coming to save you from your own mistakes.

Let me state the obvious. You should already have revenue coming in from the hundred customers you sold to, plus however many you have acquired via the marketing methods I covered in the previous chapter. So if you're profitable now, you should be able to keep it that way by focusing on the only part of the equation left to discuss: costs.

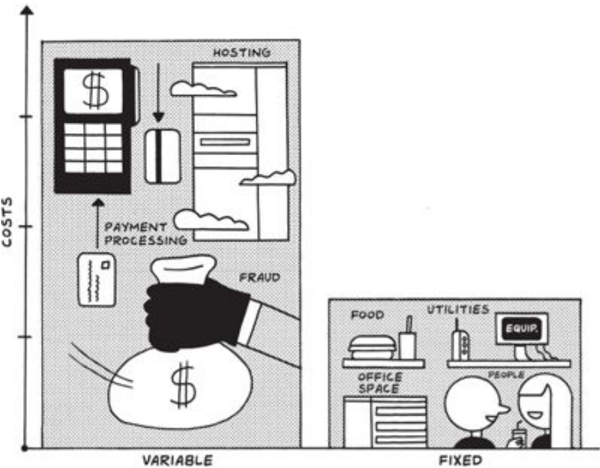

There are two kinds of costs. The first is variable cost, also referred to as the 'cost of goods sold,' or COGS: the cost associated with selling each marginal unit of product. In brick-and-mortar businesses, that includes costs like labor, packaging, raw materials, and more. For software businesses in the 1990s, COGS were non-zero because software was put onto CDs and sold in retail stores.

Things have changed a lot since then. 'Shipping' some electrons over the internet is virtually free, and the internet makes it much cheaper to collect payments online. For example, for each dollar we earn at Gumroad, we incur about 40 cents of variable costs. This 40 percent consists of payment processing fees, web hosting costs, other infrastructure costs, and fraud prevention (a necessary evil of helping people transact online).

That leaves us 60 cents per dollar. But that 60 cents isn't pure profitwe still need to pay the second kind of costs, fixed costs, which don't scale linearly with our revenue and each incremental product sold. This includes everything from our domain name to certain online services, but these aren't the main expenditures for us or for most businesses, minimalist or not. The number one fixed cost is people.

In the next chapter, we'll talk more about what it means to bring human beings into your company, but for now, let's just say that employees, their equipment, the office space they need, the internet connection, the insurance for the space, the snacks in the fridge, the electricity, and so on, cost a lot of money, and rightfully so. Starting with you, so . . .

- Pay yourself as little as possible, at least to start. You are a founder, but you are also the first employee. Treat yourself as such. Don't expect to take dividends. Instead, pay yourself an annual salary even if it is just $1, and then increase it over time as you can afford to. This will force you to do the work to get your systems set up so you can have an accurate picture of how much or how little is required to run your business, not just sell your product.

If you're worried about making a living, I get it. That's why I've recommended again and again that you start your business as a side project and use your time, energy, and ideas to grow the business to profitability before you leave your day job. Then, you can pay yourself as profits allow. In my case, when Gumroad started to work, I paid myself $36K a year, just enough to cover basic living expenses in San Francisco. Over the years, I increased my salary but tied it to the salary of the lowest-paid person at the company: $60K, then $85K. When things went sideways in 2015, I paid myself $0 for a while. Now I pay myself $120K a year.

Ultimately, you should be trying to minimize your business's burn, but also remember that the goal here is to provide yourself enough of an income to be able to focus on what matters: helping your customers solve their problems.

- Hire software, not humans. People are expensive. Software is not, usually because a lot of it is VC-subsidized in the name of growth. Take advantage of this by using Pilot or Bench instead of hiring an accountant or a CFO. Use Gusto to run payroll and benefits in five minutes. Because you are putting off hiring, you will also save money on all of the people-managing roles in your company, like an HR person

and an office manager (see below). You may be surprised how far you can get with cheap software tools. For example, you can hire a human being to follow up with new customers every time someone signs up for your service or you can use automation tools like Zapier to send a follow-up email and to add those new customers to a queue to call later.

- Don't get an office. I believed this pre-pandemic, and I, and millions of other people who weren't already convinced, believe it now. An office creates an insane amount of associated costs. Plus, you now have to manage an office. Unless you really need one, avoid it. (You can get one later if you really want it as a reward for building a meaningful, sustainable business.)

Thanks to the pandemic, there's a list of businesses a mile long that have become 'digital by default,' as Shopify founder and CEO Tobi Lutke put it, but others, like Upwork, have always thrived with distributed teams. Either way, even giants like Google, Microsoft, Morgan Stanley, JPMorgan, Capital One, Zillow, Slack, Amazon, PayPal, Salesforce, and other major companies have extended their work-from-home options post-2020, so if they don't need an office, you probably don't either.

- Don't move to Silicon Valley. Even before 2020, I would have said, 'Don't quit your job, don't move to SF, don't pass go, and don't collect $200 (from VCs).' After all, San Francisco is expensive, traffic-heavy, and not a great place to raise your children-or even a dog. Now, postCOVID, remote work is the new normal, and that means you can stay where you are. Sam Altman, the former CEO of Y Combinator, said that he was 'very excited to see SF have to compete with other cities.' Me too. Not only is it cheaper and less competitive to build your company in a smaller town or city, but it's also better for the local community, which as we've learned can pay dividends for your business.

- Outsource everything. It's all you, every day. For now. Then it's software. Eventually you and your army of robots will be at maximum capacity and you'll need help. But before you hire your first full-time employee, use freelancers. I'm not talking about exploiting good, hardworking people by paying them less than they deserve. I mean hiring future founders and other potential minimalist entrepreneurs:

offering them opportunities to learn within a functional, profitable business; paying them well; and giving them a chance to earn money while spending the rest of their time as they like-maybe even starting their own minimalist businesses themselves.

If you can use these tactics to keep your costs lower than your revenues, your business shouldn't die. Even better, you'll have something worth keeping: a profitable, sustainable, growing business serving customers. It's no longer up to the market to decide if what you built was valuable. It's now up to you not to lose it.

(This may seem overwhelming. To help, in the 'Learn More' resources at the end of this chapter, I included Gumroad's actual P&L with all of our costs, as well as simpler examples.)

In the last chapter, I described how the Doans used YouTube to grow the Missouri Star Quilt Company from a struggling mom-and-pop machine quilting shop to a global quilting empire. Looking back, the success of Missouri Star might feel like a foregone conclusion, but it wasn't obvious at the start that the company would succeed, or even survive. 'It took four years before we were profitable and could begin to pay our own salaries,' Al Doan said. 'We were doing everything ourselves, including renovating the buildings we bought, as we slowly figured out what worked both for our customers and for the company itself.'

The good news for Missouri Star was that in Hamilton, Missouri, it was much easier to keep costs lower than it would have been in Silicon Valley or another market with expensive labor and real estate. 'We started with a five-thousand-square-foot store that we thought would last us forever,' Al said, but they eventually had to separate the company's inventory into multiple shops where they could house specialized fabrics, notions, and trim. As Missouri Star expanded, the 'retail warehousing model'-in which the people who worked in the physical stores also fulfilled online ordersstarted to break down as employees could no longer simultaneously handle in-person and online sales.

The solution was obvious but also scary: To meet customer demand, Missouri Star would have to separate its retail business from its online one, which meant new warehouses, increased inventory, and more employees. As minimalist entrepreneurs, Al and his family were concerned about a radical increase in the company's variable costs, but because Missouri Star was already profitable and its revenues were growing year-over-year, they had the confidence (and the money) to support their expansion.

Al also had enough experience to know that avoiding growth and trying to maintain dysfunctional systems wasn't a good idea. 'We didn't hire a human resources person until we were at 150 employees,' he said, because it felt wasteful to pay someone to perform a function he'd done for years, 'even if [he'd] done it badly.' It took a few incidents and some intervention from a friend with an HR background for him to realize that investing in HR would be worth the cost. 'Otherwise,' he says, 'you end up with several eight-hour jobs.'

Beyond what the business has meant for the Doan family, Missouri Star Quilt Company has transformed the small town where it's headquartered. When asked about the impact on the community in 2019, Jenny Doan said that at first, 'I thought we were just sewing,' but now they employ four hundred people. In addition to growing Missouri Star, they've also started a sewing company, a knitting company, and an art company. 'We have more ideas than we have buildings at this point,' Jenny says.

The Doans' story offers many different lessons for minimalist entrepreneurs. Even if it's the goal, growth is its own challenge. Far too often, companies with plenty of talent and market potential run into trouble not because of the product or the customers but because of the unglamorous but essential parts of running the business: Operations. Finances. Human Resources. Legal. In the world of VC, where millions of dollars are thrown around on wild bets, people tend to be over-exuberant, lavishing generous perks like pool tables and free food.

Don't get swept up in what a 'successful' business is supposed to look like. Keep doing what's working, stop or improve the processes that aren't, and always, always, always keep an eye on the numbers and your ears on your customers.

Stay Focused on What Your Customers Want

The tuning fork you should resort to over and over again is quite simple: your customers.

Your customers do not want you to get bigger and grow faster. They do not care how rich you are, if you were on the Forbes '30 Under 30' list, which venture capitalists you raised money from, or how many employees you have. They want your product to improve, and your business to stick around. That's about it.

Amazon has a nice way of thinking about this: 'In every board meeting in Amazon HQ stands an empty chair. That seat represents the customer and the customer voice. So everything that is developed and created is scrutinized by the voice of the customer. That voice is what the people in the meeting room ask as if they were in the place and shoes of the customer. Why is this product important for me, what value does it bring, do we really need this service or product?'

Even though we're not trying to build Amazons, this attitude is even more important if you are at the helm of a newly profitable and growing minimalist business. As an African American father of six children, Jelani Memory, founder of Circle Media and A Kids Book About, inevitably found himself discussing racism at the table with his blended family of four white and two brown kids. Memory decided to write a book for his own children, one that would describe his experience with racism in terms they could understand.

The book, A Kids Book About Racism , was simple, with no illustrations. He proudly designed and printed one copy; it took four weeks to produce. It gave him a jumping-off point for discussing hard things with his own children, and when he showed it proudly to other friends and parents, many wanted a copy for their families. Even though he was in the midst of raising

Series B for Circle Media, the idea of starting a publishing company had taken hold of him. By January 2019, he negotiated an exit.

At that point, he started to tell everyone he knew about his ideas for A Kids Book About-these were his potential early customers, after all-and seeing their reactions and feeling 'the power of possibility in the look on people's faces' not only helped him refine the business but also validated his bigger project of publishing kids' books on challenging, empowering topics.

That energy kept him going through early challenges, including learning about publishing in general and figuring out how to manage inventory. He launched A Kids Book About in October 2019 with twelve titles, and it grew steadily but modestly until May 2020. The day after George Floyd was killed by police on May 25, 2020, 'A Kids Book About did as much in sales as it had the whole previous month. And it didn't slow down,' Memory said. 'The following day, sales went up 2x, and the day after, went up another 2x and held steady. So, within the span of 10 days, A Kids Book About saw north of $1 million in revenue.' Their inventory was supposed to last the rest of the year, but they sold out of every single one of their titles but two.

Those sales figures validated Memory's belief in the product he was offering and in the possibility for growth within a changing world. He says, 'There is a misconception that money or investment confers validation and permission to do things in conventional and expensive ways, but that's not true. It's about product, revenue, and traction. Most of all, customer affection is the permission you need to grow.'

If you stay focused on what drives sales and what excites your customers, then you'll know how to grow; they'll tell you. And if you pay attention as you go, even as you do unwittingly make unforced errors, it will be your customers (or the lack thereof) who will show you how to get back on track, far before you would have otherwise noticed.

Finally, be diligent about the essentials. It's easy to excuse sloppy practices when you're growing and feel overwhelmed, but that's the moment when you need to be most disciplined about how you spend your time and money. Not just because of the implications for your bottom line but also because nothing brings a business to a screeching halt faster than a legal problem or a break in the supply chain.

Paychecks need to go out on time, and it's on you to avoid any legal, financial, or operational complications that might sink the ship. Vendors need to be registered in the system and paid promptly. IT security needs to be buttoned up tight, particularly around user privacy. You need to run a good, clean business to establish and uphold your reputation with employees, vendors, and customers. Chances are, however, that one or more of these areas lies outside your area of experience. You probably lack even the basic knowledge to hire the right help. That's okay. We'll talk more on hiring in the next chapter.

Until then, good news: Your customers can connect you to people who can help, especially if you're open with them about what you need. They're already incentivized to support you, because they use your product and want to make it better. And there's another way to get them even more involved with your success: turning them into owners.

Raise Money from Your Community

Growing businesses, even minimalist businesses, may need capital at some point. Raising money can make sense, once you know how you would spend it to improve the lives of the customers you already have. Shopify, for example, and 1Password raised money several years into their lives. Because they were both profitable when they did it, they were able to keep their visions aligned and their dilution low, and retain control of their companies.

If you do choose to go the venture capital route (Hit me up! shl.vc), profitability will give you leverage in those negotiations. But there are also new ways to raise money, ones that preserve your ownership and empower your customers.

I don't just mean new venture capital funds such as Calm Company Fund (disclosure: I am an investor), and Tinyseed Fund, which are looking to invest in more sustainable, perhaps minimalist, businesses. These firms are building a portfolio with a higher hit rate, allowing them not to overoptimize for finding the single company that returns their whole fund. But they are far from the norm.

What I am mostly talking about here is a totally new way to raise money from your customers and your communities: Regulation Crowdfunding.

In 2012, President Obama signed the JOBS Act into law. This bill, among many other things, included the ability for private companies like Gumroad to sell shares to the general public, making it possible for almost anyone to invest in the business. On March 15, 2021, the legal limit for regulation crowdfunding went from $1.07 million to $5 million. These new rules also allow for 'testing the waters,' allowing companies like Gumroad to see how much demand there is to invest in the company before committing to a crowdfunding campaign.

I believe that crowdfunding will reorganize the funding landscape. There will always be a place for venture capitalists, but who better to fund a business than its customers, who understand how valuable its offering is? And once founders can vet demand before committing, we should see the numbers skyrocket.

In the old way, the number one downside of raising money was that you created two distinct sets of stakeholders: your investors and your customers. This new practice will allow entrepreneurs to minimize complexity by turning customers into investors. All of a sudden, you have a single group of people you are serving: your community.

I can speak from experience: On March 15, 2021, I used Regulation Crowdfunding to allow some of Gumroad's creators to become partowners. In 12 hours, we raised $5 million from more than 7,000 individual investors. Now we have thousands of our creators as our investors too, keeping our interests more cleanly aligned.

For the businesses that neither need to bootstrap completely nor want to go the venture-backed path, I'm hopeful that Regulation Crowdfunding will offer a middle ground. But the ultimate long-term goal remains profitability

(read: sustainability). Once you're in control of your destiny, you should never let it go.

Build Profitable Confidence

I know I've said over and over again that profitability is the metric that matters most to your business. That's because profitability is a superpower. If you rely on VCs for capital, like we did in the early days, you rely on outside forces to be successful. When they pull the plug, you have no more electricity. Your backup generator will last a certain amount of time, then run out too.

Profitability gets you off the grid, allowing you to grow mindfully with unlimited runway. You can take your time and make thoughtful decisions that move you toward the right targets at your pace, not someone else's. As some Navy SEALs say, 'Slow is smooth and smooth is fast.'

Chris Savage, CEO and cofounder of Wistia, a video and podcast marketing platform, calls the resulting sense of conviction 'profitable confidence.' In 2017, Savage and his cofounder, Brendan Schwartz, realized that their efforts to scale and grow quickly had not only made their work less creatively interesting, but had also made them unprofitable. By slowing down, they figured out how to trust their instincts again-and wound up more profitable than ever.

For Wistia, being profitably confident means that Chris and Brendan know they will live no matter what they do. It allows them to pursue ideas at their own pace, and that frees them up so that every single thing doesn't have to work immediately (or even at all). They don't have to bet the company anymore if they want to try something new, and they can wait years for something to pay off.

This feels great, because you can truly invest in the stuff that you think will create a lot of value for your customers, not just the stuff that will 'move the needle' on your top-line growth metrics as soon as possible, so that you can raise the venture capital you need to keep going.

When you are profitable, you can take your time. You can talk to customers and really make sure you understand their problems before you attempt to solve them. Then you can iterate on your solution over and over again until you're really happy with it even if you take years to do it. You could even show customers and get their feedback again and again, like we often do.

Since you are running on your own steam, your runway will now last you forever. You will not die unless you do something stupid. This means you need to hire slowly, not ambitiously. You should also avoid irreversible decisions like getting a multiyear office lease. Moving slowly will mean you can ship more thoughtfully because you'll have the time and space to learn about yourself, your customers, and your market. It will also give you a clear view of the road ahead. You will be able to detect bugs in your product and systems before they affect your customers. You can test your software in private beta with customers, or behind a waitlist. You can make sure it's good enough before you give it a wide release. This way, your customers continue to appreciate every thoughtful addition- or subtraction -you make and to love your product without worrying about the mistakes that accompany quick changes and rash decisions.

Overcommunicate with Your Cofounder

Once your business is too well run to fail, there's one more failure point to address: you. Your business won't run out of money, but you may still run out of energy.

One of the fastest ways to drain your enthusiasm and to lose steam is a cofounder fight. According to Paul Graham, founder disagreements are par for the course, and 20 percent of those situations escalate until one founder departs the company.

No one gets married expecting to divorce, and most cofounders don't anticipate that things won't work out either. But ultimately, relationships are relationships, and it can be useful to apply frameworks for personal relationships to professional ones if they apply.

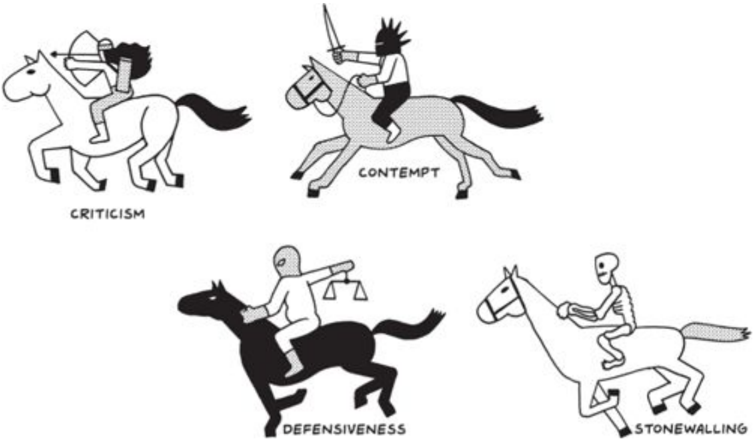

Drs. John and Julie Gottman, well-known couples therapists, say they can predict the end of relationships using 'The Four Horsemen of the Apocalypse,' their name for four types of communication styles that start to appear in a relationship: (1) criticism, (2) contempt, (3) defensiveness, and (4) stonewalling. While some founders succeed at tackling their conflicts head-on and eventually rediscover common purpose and mission, others never do, and one founder will move on.

In Startupland, this isn't necessarily a bad thing. Startups are encouraged to 'fail fast,' and founders often cycle through several teams at the same time they're cycling through ideas.

But there's also a lot of truth when people say, 'It's harder to divorce your cofounder than your spouse,' so if you want to give your business the best chance at success, approach the relationship with your cofounder(s) like a marriage. Think about the following before you team up for the long haul:

- Do not start a relationship with someone unless you really, really trust them.

- Do introduce vesting so that each of you earns your stock over several years.

- Do make sure you are aligned on your values, what you want to build, and how you want to build it.

- Do not ignore the possibility that one of you may leave. Plan for what a successful exit from the business may look like.

- Do have the hard conversations as early as you possibly can. Just like there's no point in dating someone for five years before you figure out if they want what you want, early in any serious professional relationship, it is important to explore and understand each other's values and

ambitions. Because hard conversations get harder the longer you wait to have them. Here are some questions worth asking your potential partners:

- What does a happy relationship look like?

- What does success for this business look like?

- What does an exit look like?

- How fast do we want to grow?

- Why are we starting this together?

Have these hard conversations again and again. Think about specific checkins to reevaluate these goals so that disagreements don't fester silently, and make sure that whatever path you plan on taking, you're on the same page about it.

Maintain Your Energy and Sanity

The conventional wisdom is that there are two kinds of startup founders: On one end of the spectrum, you run a lifestyle business and lounge on the beach all day, and at the other, you work 24/7, only stopping to eat or sleep when absolutely necessary and sacrificing exercise, rest, family, the outdoors, and whatever in your life gives you pleasure and sustenance.

There's a lot of real estate between those two extremes, and just like your business needs to change and to grow to keep from getting stagnant, so do you as a human being. I'd be lying if I said that being a minimalist entrepreneur doesn't take a lot of hard work, but it doesn't have to be an allor-nothing proposition.

I can speak from experience, as I've changed my mind about what I wanted out of Gumroad quite a few times. For the first several years of Gumroad's life, I was chasing unicorns. Then I right-sized the business to profitability, and today it's one of a few things I am working on, like this book. Generally, I don't let my business make me too happy, so that it can't make me too sad. But it took years for me to get here, and the kind of people who wanted to work on Gumroad at each phase were very different. I basically had to rebuild the whole team from scratch.

When you're growing at all costs, it's easy to avoid these conversations. It's easy to justify not having them too: You're all focused on growth, and these conversations aren't helping you grow in the short term. But in the long term, as your business morphs like every business does, you need to have them. Or they'll happen to you when you least expect them to, and that's a lot less fun.

To be clear, this isn't about scaling back your ambitions in order to make your business work. It's about aligning the ambitions you have for yourself and your company with the ambitions your customers have for themselves. Because I'm not trying to build a billion-dollar business at all costs, my focus now is on creating more creators and business owners.

And frankly, you often can't grow faster if you try. I've worked sixty hours a week for years on end, and I've worked four hours a week. For better or worse, Gumroad grew at its own pace, and the number of hours I worked didn't seem to have much of a correlation. I think you'll find the same is true for you: Your company will grow as quickly as your customers determine it will grow. For us, that was 15 percent in 2017, 25 percent in 2018, 40 percent in 2019, and 87 percent year-over-year in 2020.

It taught me to be wary of thinking I always needed to do more, earn more, or grow more than I needed to. Once I came to terms with the reality that I couldn't control everything, it got a lot easier to move forward. Instead of pretending to be a product visionary and trying to build a billiondollar company, as if it were within my control, I could focus on making Gumroad better for our existing creators.

Some say that you need to grow like crazy, because 'if you don't get big, someone else will eat you.' As if companies were fish.

This is wrong. The vast majority of small businesses are never eaten. Big fish want to eat other big fish. In fact, the longest-lived businesses in the world are also some of the smallest. They are restaurants, hotels, construction companies, and more. Many of them are family firms, or small to midsize enterprises content with steady evolution of their niche and a passionate multigenerational customer base. Something to aspire to!

Maybe you already know this. Maybe that's the business you already aspire to build. If so, I'm glad. But it wasn't obvious to me when I started out, and I see these ideologies pervade and persist in social media, within headlines, and on TV.

One more economics lesson to wrap up: There's no free lunch. Once you have it, you will feel the pressure to spend money more loosely. Keep in mind the lessons we covered in this chapter as you start to spend your customers' money, making sure you're treating it as if it were your own. Instead of hiring like crazy, hire when it hurts. Instead of getting a fancy office, work out of a fancy coffee shop. When you do spend money, see how it affects your burn rate and your runway.

At this point, you know how to keep things going and growing. You're ready to start hiring and building operational excellence within your company to scale up. That's what we'll cover in the next chapter.

KEY TAKEAWAYS

- Seek 'profitable confidence': Infinite runway will maximize your creativity, clarity, and control. This is simple (spend less than you make) but not easy.

- How to spend less: Do less. Don't move too fast, don't move to Silicon Valley, don't get an office, don't get too big. Grow as fast as your customers want you to-and are paying you to.

- If you raise money, think about raising it from your community and turning your customers into owners.

- Ultimately, most founders run out of energy before they run out of money. Maintain your energy and sanity, and that of your cofounders and coworkers, by realigning early and often on what really matters.

Learn More

- Follow Chris Savage, cofounder and CEO of Wistia, on Twitter (@chrissavage), and read his post on profitable confidence here:

https://wistia.com/learn/culture/profitable-confidence-how-to-build-abusiness-for-the-long-term.

- Read about 'The Four Horsemen' by the Gottmans, starting here: www.gottman.com/blog/the-four-horsemen-recognizing-criticismcontempt-defensiveness-and-stonewalling/.

- Check out the Gumroad crowdfunding campaign here: https://republic.co/gumroad.